By Max from UNFTR

Watch the video report of this article below or click here.

Healthcare in the United States is some of the best in the world.

If you can afford it.

Health coverage in the United States is some of the worst in the world.

If you can afford it.

Those are the first and last lines of this story. Our job today is to fill in the blanks in between with a sense of urgency because new studies just released revealed how the Trump administration’s new budget bill is likely the final death blow to a system already teetering on the edge.

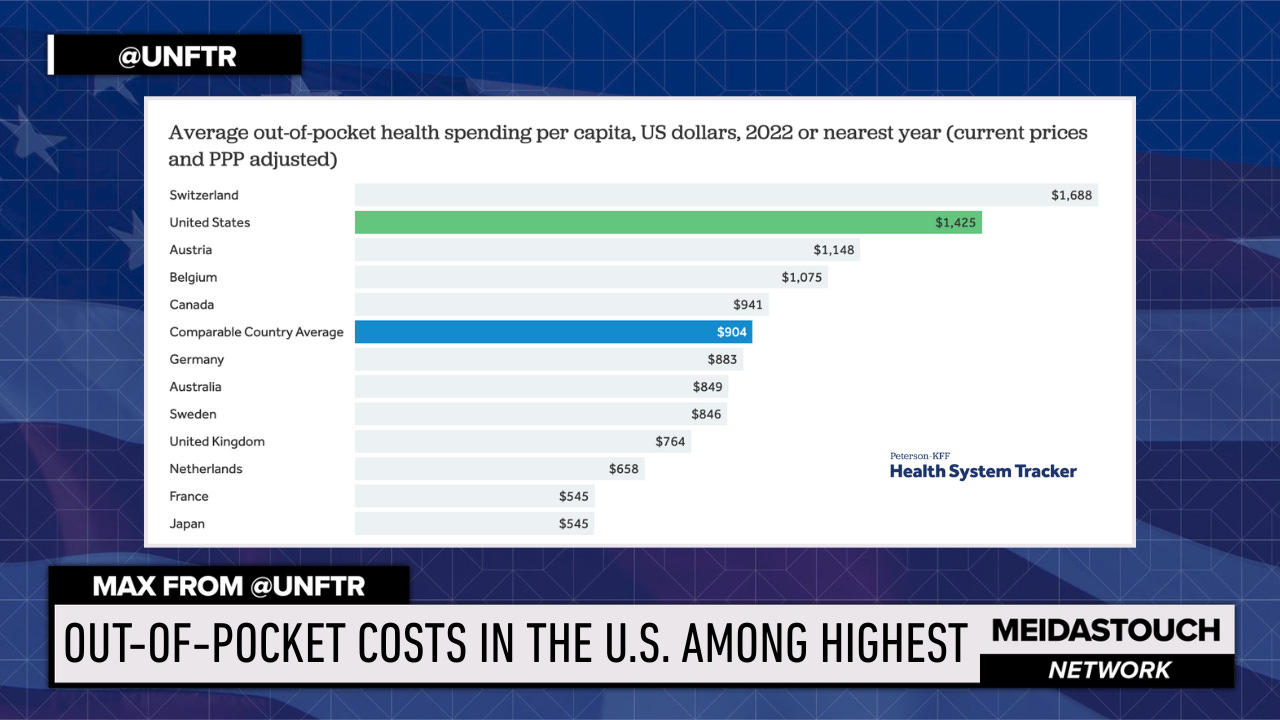

The American healthcare system is already in crisis. Outcomes aren’t better than other peer nations, and in some cases it’s far worse, despite the fact that we have the highest cost of coverage and the second highest out-of-pocket costs in the world.

So while we’re going to go through how the new GOP legislation is about to destroy the fragile healthcare ecosystem starting in 2026, it’s important to be honest about our starting point.

That said, literally every delivery source of healthcare coverage is going to be affected. Whether you get your insurance from the ACA exchange, the government or your employer, costs are going up. By a lot. That’s the takeaway from the GOP approach to healthcare, which is all rooted in the GOP promise to “repeal and replace.”

Ascribing blame can be satisfying but once again we have to be honest that the blame is spread far and wide when it comes to the system we currently have in place. But there’s no question that the Republicans’ tear-it-all-down strategy is going to cause undue and unnecessary pain and suffering for the vast majority of American households. And they have neither a plan nor the intention to solve this crisis.

To the GOP it’s as simple as “make more money or just don’t get sick”.

This also means the Democrats have the opportunity of a lifetime to finally see the solution that’s been sitting in front of them for more than six decades.

We're about to witness the biggest healthcare crisis in decades, and it's entirely manufactured. Right now, as we speak, millions of Americans are losing their Medicaid coverage due to the draconian work requirements embedded in what Republicans euphemistically call the "One Big Beautiful Bill." But here's what they don't want you to know: this isn't just going to hurt the people who lose coverage—it's going to devastate everyone.

When millions of people get kicked off Medicaid, state budgets don't just magically fix themselves. States are going to scramble to fill that gap, and guess what happens next? The entire private insurance market gets slammed with higher costs because it reduces the risk pool required to make insurance affordable.

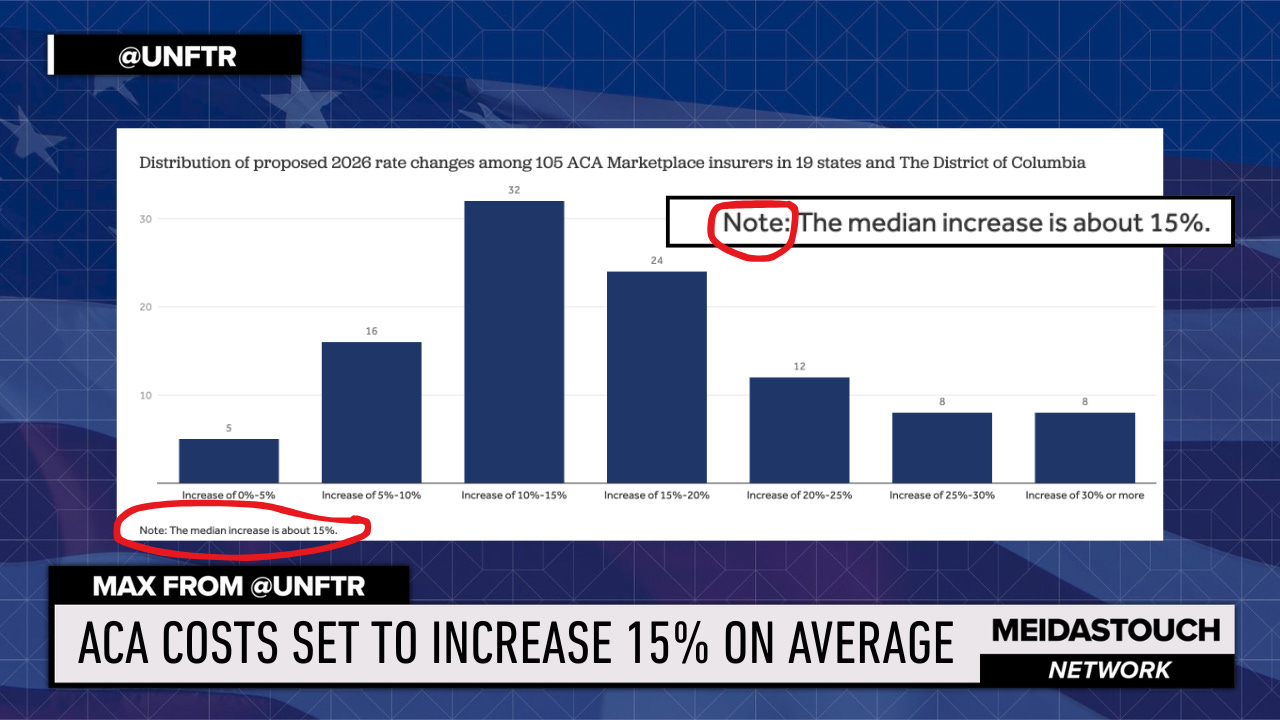

We're already seeing insurance companies request premium increases of 15% or more for 2026—the largest increases we've seen since 2018. And that's before the full impact of these Medicaid cuts hits.

This is the perverse reality of building a healthcare system around private insurance and employment-based coverage. When one part fails, the whole rickety structure starts to collapse. And the people who suffer? Working families, small businesses, and anyone who dares to get sick in America.

But here's the thing—this crisis could be the catalyst for the solution we should have implemented decades ago. Because while other developed nations figured out long ago that healthcare is a public good, not a profit center, we've been trapped in a system designed to extract wealth, not deliver care.

Private healthcare markets are built on fundamentally perverse incentive structures. You cannot have a system designed to help people stay healthy—which requires fewer medical interventions—when that same system is designed to generate profits from more care and expensive interventions. If fire departments made money every time they put out a fire and their jobs depended on it, there would be a lot of arsonists in the department.

Of course, we don’t need that ridiculous hypothetical scenario to drive home the idea of perverse incentives. Take the private prison industrial complex that thrives on recidivism and punitive laws for minor offenses that put people behind bars for less and for longer. Or a healthcare system that incentivizes insurers to deny claims and providers to make as much money on everything from routine visits and prescription drugs to hospital stays.

That's why every other developed country treats healthcare as a central government responsibility. It's not a fringe progressive idea—private insurance is the fringe idea, and we're about to see exactly why it's failing so spectacularly.

The American healthcare system isn’t some grand design based on careful policy analysis. It was an accident of history that we've been too stubborn to fix. During World War II, wage freezes meant employers couldn't compete for workers with higher pay, so certain ones— most notably unions—started offering health benefits instead. What began as a wartime workaround became the foundation of our entire system.

When Lyndon Johnson created Medicare and Medicaid as part of the Great Society, it was supposed to be the beginning, not the end. Medicare and Medicaid were designed as the first steps toward universal coverage—a way to prove that government-run healthcare could work by starting with the most vulnerable populations: seniors and the indigent.

The plan was to gradually expand coverage to everyone. But the implementation costs were higher than expected, and political resistance was fierce. Believe it or not, it was the American Medical Association that fought it tooth and nail, convinced that government involvement would destroy the profession. They were wrong, of course—Medicare became wildly popular and efficient—but the damage was done. The momentum for universal coverage stalled.

It would be years before we had another shot under Jimmy Carter. Ted Kennedy was pushing hard for a comprehensive national health plan, but the relationship between Kennedy and Carter was so toxic that they couldn't work together. Another ‘Democrats eating their own’ moment when personal politics killed what could have been the moment we joined the rest of the developed world in treating healthcare as a right.

Once Ronald Reagan took office, the window closed completely. The Reagan era ushered in the philosophy that government is the problem, not the solution, and private markets can solve everything. The healthcare industry, smelling opportunity, began its massive expansion. Insurance companies grew larger and more powerful. Hospital systems consolidated. The pharmaceutical industry discovered it could charge whatever it wanted.

Instead of a rational system designed to keep people healthy, we built a labyrinthine extraction machine designed to generate profits. And we've been living with the consequences ever since.

This employment-based system creates massive vulnerabilities. When people lose their jobs, they lose their healthcare. When companies can't afford rising premiums, they cut benefits or drop coverage entirely. We need elaborate safety net programs like Medicaid precisely because our primary system is so unreliable.

But here's the irony: every time we try to patch the system with safety net programs, conservatives complain about government spending and dependency. They've created a system that requires government intervention, then complain about government intervention. It's maddening.

The next major attempt at healthcare reform came under Bill Clinton in the early 1990s. Recall that it was actually Hillary Clinton who led the charge, developing a comprehensive plan that would have provided universal coverage while maintaining a role for private insurance. It was complex and in retrospect looked a lot like Obamacare.

The response was swift and brutal. Newt Gingrich and the Republican coalition in Congress launched an all-out assault on the plan, painting it as government overreach and socialized medicine. The insurance industry spent millions on the infamous "Harry and Louise" ads, featuring a couple worrying about government bureaucrats coming between them and their doctor—while completely ignoring the insurance company bureaucrats already doing exactly that.

The Clinton plan died, and with it, any hope of meaningful reform for another generation.

Share

When Barack Obama came into office, he faced the same basic choice: push for a true universal system or try to work within the existing private insurance framework. He chose the latter, and the result was the Affordable Care Act—a plan that, ironically, was originally developed by the conservative Heritage Foundation and implemented in Massachusetts by Mitt Romney. And if Heritage sounds familiar, they were the lead sponsor of Project 2025.

Think about that for a moment. Obama's signature healthcare achievement was based on a conservative think tank's plan designed to preserve the private insurance market while forcing people to buy coverage through mandates. It was literally designed to avoid creating a government-run alternative that might compete with private insurers.

The ACA did accomplish some important things. It brought millions of people into coverage through the exchanges, expanded Medicaid in most states, and eliminated some of the worst practices of insurance companies like denying coverage for pre-existing conditions. These were genuine improvements that saved lives and prevented bankruptcies.

But the fundamental structure remained intact. We still had a system designed to generate profits, not health outcomes. And predictably, costs continued to rise. Insurance companies found new ways to extract profits—raising deductibles, narrowing networks, and increasing out-of-pocket costs. Pharmaceutical companies continued their relentless price increases. Hospital systems kept consolidating and raising prices.

The ACA slowed the rate of cost increases temporarily, but it couldn't solve the underlying problem: when your system is designed to maximize profits rather than health outcomes, costs will always spiral upward. You can't regulate your way out of a fundamentally misaligned incentive structure.

Healthcare providers, now guaranteed more paying customers through the exchanges and Medicaid expansion, had every incentive to raise prices. They knew insurance companies would pass those costs on to patients and taxpayers.

The ACA essentially guaranteed a larger customer base for an already dysfunctional market.

From the moment the ACA passed, Republicans made destroying it their primary mission. They voted to repeal it over 60 times in the House. They challenged it in the Supreme Court multiple times. They refused to expand Medicaid in their states, leaving millions of their own constituents without coverage out of pure spite.

When they finally gained control of government in 2017, they came within one vote—John McCain's famous thumbs down—of repealing the entire law without any replacement plan. Think about that. They were willing to throw 20+ million people off their health insurance with no alternative, just to score political points.

When outright repeal failed, they shifted to death by a thousand cuts. They eliminated the individual mandate penalty, weakened enforcement of insurance regulations, and created junk insurance plans that provided virtually no real coverage. They sabotaged the system they couldn't destroy outright.

The COVID pandemic provided a brief reprieve. The Biden administration enhanced the premium tax credits that made coverage more affordable, and enrollment in the exchanges surged. Millions of people gained coverage, and for a moment, it looked like the system might stabilize.

But costs kept rising anyway. Despite more people joining the risk pools, insurance companies continued raising premiums. Why? Because the fundamental incentive structure hadn't changed. More customers just meant more opportunities to extract profits.

And the profiteering became increasingly sophisticated. Pharmacy Benefit Managers—middlemen who were supposed to help control drug costs—became massive profit centers themselves. The three largest PBMs took in $604 billion in 2023 alone while manipulating drug formularies to maximize their own profits.

Insurance companies developed algorithms to automatically deny a certain percentage of claims, knowing that most people won't appeal. They created networks so narrow that patients often couldn't find in-network specialists. They raised deductibles so high that people effectively had no coverage for anything but catastrophic events.

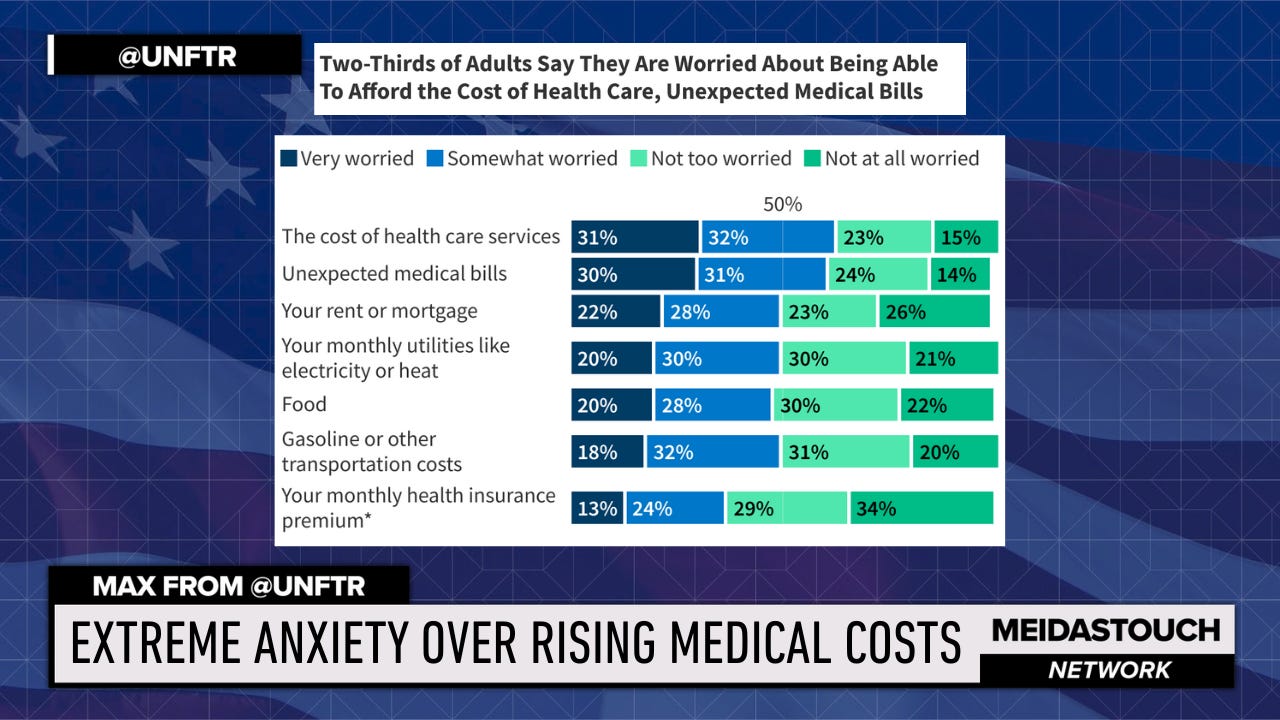

The result is national anxiety with two-thirds of adults saying they’re worried about being able to afford the cost of healthcare. Forty-one percent of American adults currently have medical debt. One in four people say they or a family member had problems paying for healthcare in the past year. About one-third of adults have skipped or postponed needed care because of cost.

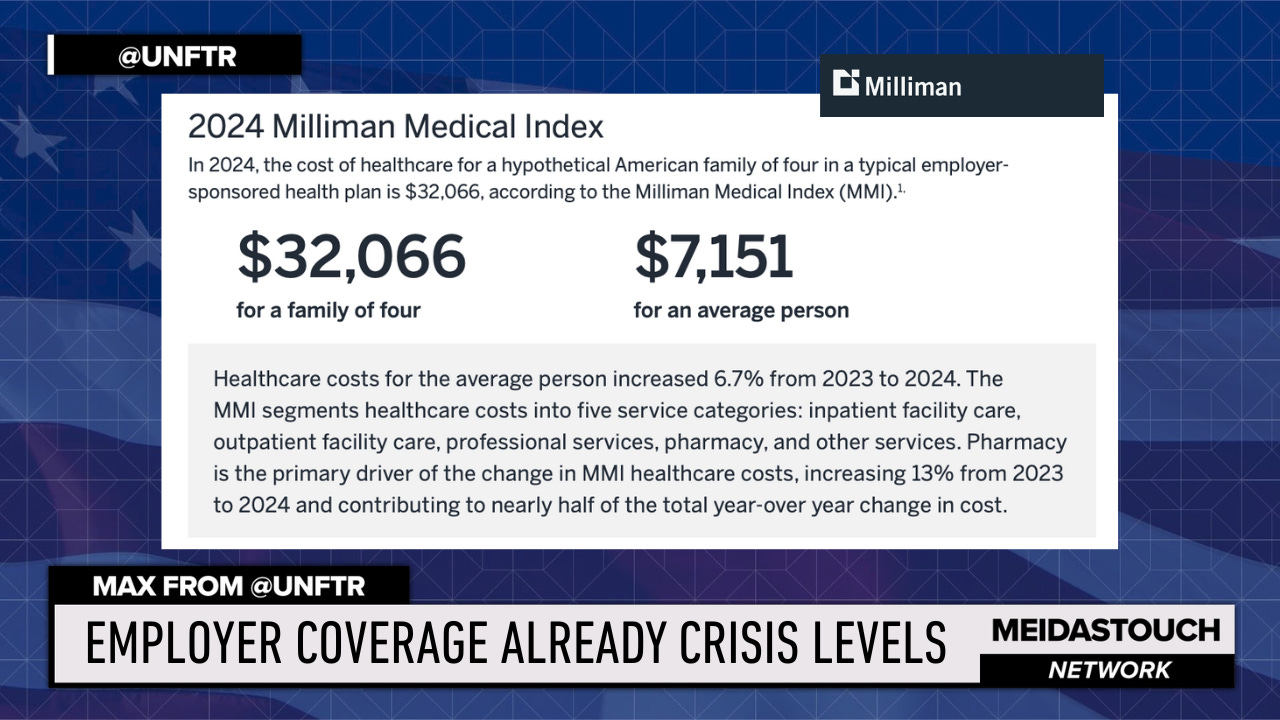

Even among those with coverage as you see here, the numbers are already off the charts. I mean, $32,000 a year for family coverage and $7,000 for individual coverage? On no planet do any of these numbers make sense. It’s unsustainable for literally everyone involved.

This isn't a healthcare system—it's a wealth extraction scheme with medical care as a side effect.

Now we're about to see this dysfunctional system pushed to its breaking point. The new KFF analysis makes it crystal clear: healthcare costs are about to explode beyond anything we've seen in recent years.

Insurance companies are requesting premium increases of 15% or more for 2026—the largest increases in more than five years. But that's just the beginning. When the enhanced premium tax credits expire at the end of 2025, out-of-pocket premium payments for subsidized enrollees will increase by over 75%.

And here's where the cruel mathematics of insurance markets kicks in. When premiums spike, the first people to drop coverage are the healthy ones who figure they can risk going without insurance. That leaves the insurance pools with sicker, more expensive patients, which drives costs even higher in a vicious cycle.

The Congressional Budget Office estimates that letting the enhanced subsidies expire will increase the number of uninsured by 4.2 million people. But that's just the direct effect. As healthy people leave the market, the risk pools get sicker and more expensive, potentially triggering even more people to drop coverage.

Meanwhile, the One Big Beautiful Bill is throwing millions more people off Medicaid through work requirements and other restrictions.

As we’ve noted before on Meidas, when these people lose Medicaid, they don't just disappear. They show up at emergency rooms when they get sick, and hospitals are legally required to treat them regardless of ability to pay. Those costs get passed on to everyone else in the form of higher prices for insured patients.

State budgets, already strained by reduced federal Medicaid funding, will be forced to cut other programs or raise taxes to make up the difference. Either way, working families pay the price.

Corporate America is already struggling with healthcare costs. The average family premium for employer-sponsored coverage has been rising faster than wages for years. Companies are responding by shifting more costs to employees through higher deductibles and co-pays, or by dropping coverage altogether for part-time workers.

So let's be clear about who wins and who loses in this scenario. The losers are sick people who can't afford care, hospitals and providers who won't get paid for treating uninsured patients, companies struggling with rising healthcare costs, and basically every American who isn't a shareholder in an insurance or pharmaceutical company.

The winners? Insurance companies and pharmaceutical companies who can manage risks and manipulate reimbursements to maintain profitability no matter how many people suffer. They've built a system where they literally profit from human misery, and they're very good at it.

Healthcare costs are reaching maximum pain levels for individuals and families, with stunning increases starting next year. We're creating a system where only the wealthy can afford to get sick, while everyone else either goes without care or goes bankrupt trying to pay for it.