Trump Crypto and SPAC SCAM Revealed

Trump is set to make billions through a backdoor Crypto scheme involving Truth Social.

By Max from UNFTR

I have a story for you. It’s a grift inside a con inside of a shell game. Our protagonist is none other than Donald John Trump, though nothing I’m about to tell you about his con of a lifetime is illegal. And that’s the point. Oligarchy is real, and this story illustrates just how rigged the game is against the American people.

Our story begins with how Trump’s media company, Trump Media & Technology Group Corp., was able to purchase $400 million of its own shares. We’ll talk about the why and how of it all, what the company does, and how it feeds into the Wall Street shell game of stock buybacks that are propping up the equity markets right now.

The Truth is Out There

There’s a very good chance you’re not on Truth Social, the centerpiece asset of the Trump Media Group. X has 300 times the number of daily users. Even BlueSky has ten times the number of daily users. And yet, the company that owns it is so well capitalized that it was able to buy back $400 million of its own shares, and it raised more than $3 billion when it went public. All despite the fact that Truth Social isn’t really a business.

When Trump Media went public with only Truth Social to hang its hat on, there was an initial frenzy in the market because there was speculation at the time that Trump might be elected to a second term. It was a longshot gamble that hasn’t paid off for anyone, really—except for the cast of charlatans behind the issuance and, of course, Trump himself.

Despite the chest-thumping about great technology and Truth Social taking over the social media world, the reality was the complete opposite. Gamblers and Trump sycophants poured money into the stock anyway, but savvy investors knew from Jump Street that there was no “there” there.

A year later and the numbers don’t lie.

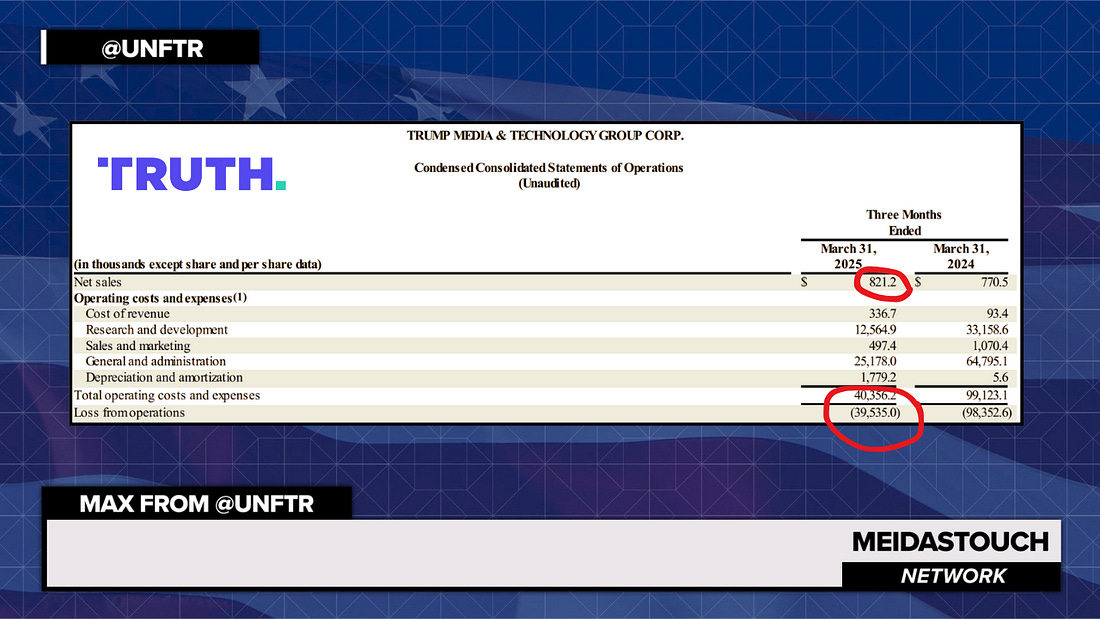

|

This is ripped directly from the company’s most recent quarterly filing with the SEC. Net sales for the quarter ending March 31 of this year show that Trump Media brought in a paltry $821 thousand in revenue. (For comparison’s sake, Meta’s Q1 revenue was $42 billion.) This puts Trump Media on pace to hit $3.2 million for the year. Even more ridiculous is that to pull in that $821K in revenue, it cost the company $40 million.

So it lost $39 million for the quarter.

Trump’s Truth Social has been a disaster from the beginning. First off, it’s lousy tech. Second, it’s bleeding cash, and there’s no appreciable revenue model in sight. So it begs the question: how on earth was this company even able to go public in the first place? Here’s where our story really begins and the first scam is revealed.

Truth Social’s holding company, Trump Media, was a failure in search of a sugar daddy. And boy, did it find one. Trump Media merged with a company called Digital World, a startup investment vehicle referred to as a SPAC, which stands for Special Purpose Acquisition Company. These are publicly traded investment vehicles created for the sole purpose of acquiring or merging with an existing private company, effectively taking it public without going through the traditional IPO process.

SPACs have been around for several decades but gained popularity in the early 2000s. They’re referred to on Wall Street as “blank check” companies because that’s essentially what they are—money in search of an idea. Even though the first one was launched in 1997, it wasn’t a popular vehicle because of the risks associated with it. It wasn’t until a tech bro named Chamath Palihapitiya got involved that the SPAC world was set ablaze.

What Chamath and others figured out was that high-profile people—from celebrities to Wall Street titans—could skip the hard part of going public and get listed with just a filing and a promise. If they could get Brad Pitt to fart in a paper bag, they could get people to invest in it.

The initial investors come in at very favorable terms, typically with something called warrants, which allow them to purchase severely discounted shares of the SPAC once it’s listed on an exchange. The trick here, however, is all about timing.

The SPAC usually has a limited amount of time—between 12 and 18 months—to identify an acquisition. The funds are held in a trust account until the SPAC identifies a target company to acquire. Once a target is identified, the SPAC undergoes a merger or acquisition, effectively taking the target public. If the SPAC fails to complete an acquisition within a specified timeframe, it must return the funds to its investors.

It should be noted that regulators hate these vehicles. Like every other public company, SPACs are subject to regulation by the Securities and Exchange Commission (SEC) and other regulatory bodies. And with each passing year, the SEC is making it more and more difficult for SPACs to maneuver because, well, for the most part, they suck.

For example, literally none of Chamath’s SPACs ever worked out. In fact, they’ve been a disaster. The ones that survived the holding period are down significantly. Others either closed or never even got off the ground, which has made Chamath somewhat of a pariah in investment circles.

Digital World was able to meet the first threshold by merging with Trump Media, and that’s how it was able to hit the ground running on the exchange. But at some point, the company also has to perform. Otherwise, it’s just a regular old pump-and-dump scheme.

Once again, the chief grifter in charge had to pony up little, if anything, other than his name. In return, he receives extremely favorable terms on this investment of nothing. According to some analysts, just the cash portion of what he received once it went public was in the hundreds of millions. And because he’s such a stable genius who surrounds himself with only the best people, you can imagine the clown car of shysters who got this thing off the ground.

The original CEO was a guy named Patrick Orlando, whose impressive resume included a defunct biofuel company in Peru, a deal with Venezuela to finance tugboats, and another venture in China. The only real record of his accomplishments lay in the trove of lawsuits he typically left in his wake, but he had enough to muster up a $25,000 investment into Digital World, and he knew how to organize a SPAC. His stake was purportedly worth around $600 million when he was ousted from the company.

Then there’s Luis Orleans-Braganza, the founding CFO of the company. He was a vocal supporter of Donald Trump and maintained close ties with Jair Bolsonaro. Oh, he’s also no longer with the company.

We’ve got Bruce J. Garelick, who was on the founding board. The SEC filed charges against him for trading in advance of the SPAC announcement. Another fancy term for that would be “insider trading.”

Rounding it out: founding board members Justin Shaner and Brian Shevland. Shaner was subpoenaed by the SEC last year, and Shevland was suspended by the SEC from acting as a broker.

Only the best people.

Attack of the Buyback

Now that you know how they pulled off taking Truth Social public—despite the fact that it has almost no revenue, loses hundreds of millions of dollars, is built on horrible technology, and has no plans to actually become a real business—let’s talk about that $400 million stock buyback, because this is part of a trend that has wider implications for the economy.

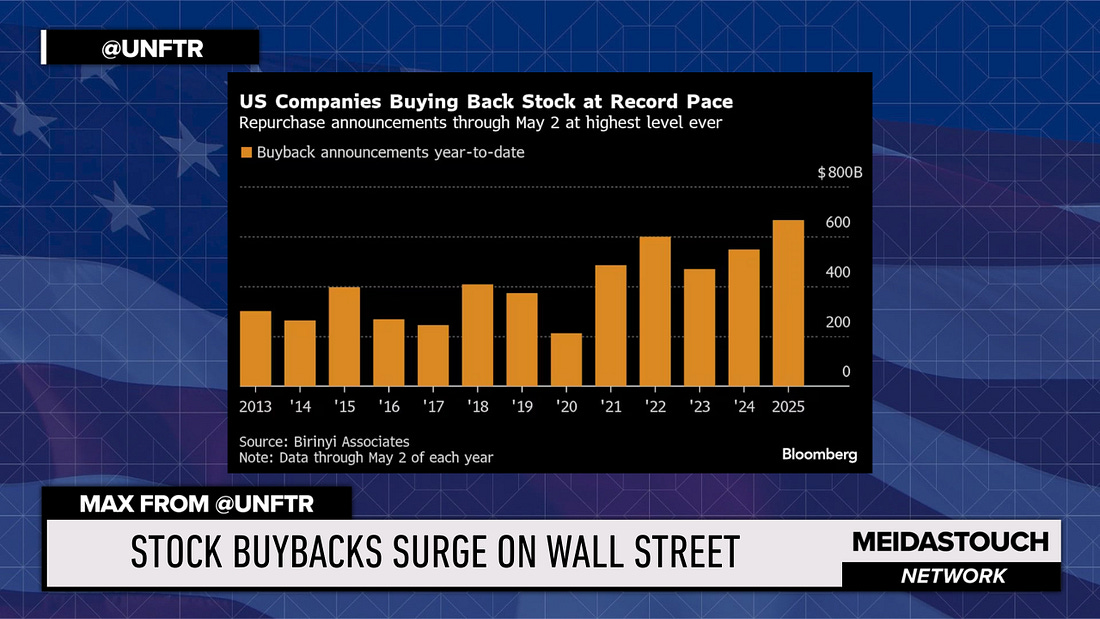

Buybacks are very much in the news today because in April, U.S. corporations announced a staggering $233.8 billion in stock buybacks—the second-highest monthly total ever recorded.

|

But unlike previous buyback bonanzas, this isn't a sign of economic strength or corporate confidence. Quite the opposite. This time, it's a bit of a red flag.

Companies aren't plowing this cash into their businesses because they see amazing growth opportunities. They're not investing in innovation, workers, or expansion. Instead, some argue they’re spending billions to prop up their own share prices in a cynical bid to boost executive bonuses tied to stock performance.

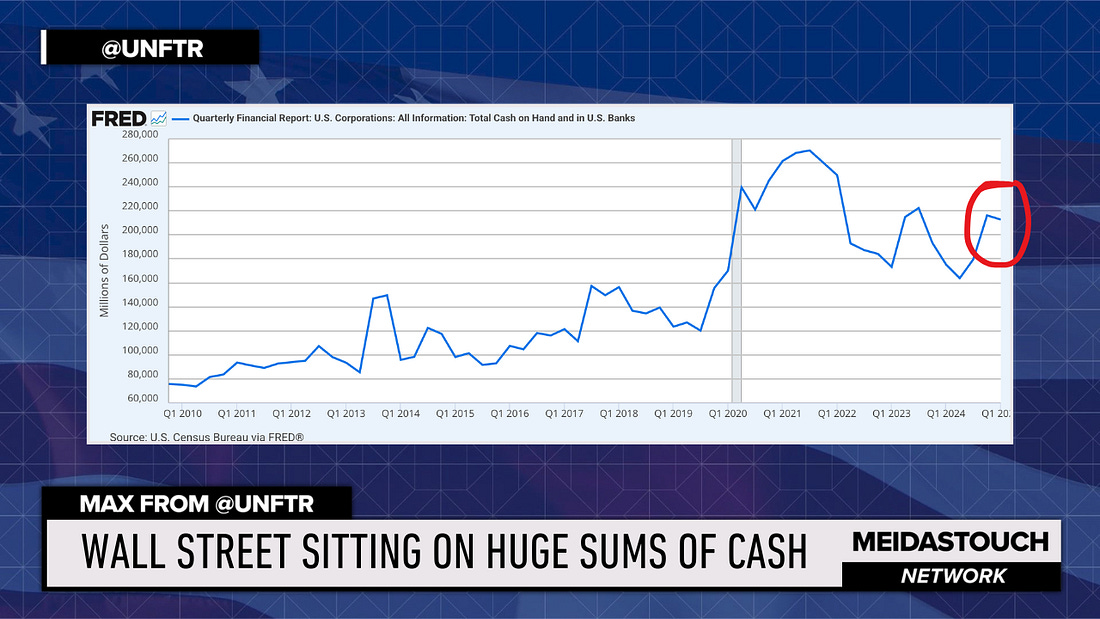

Take a look at this chart from the Fed.

|

What you’re looking at is the mountain of cash that Corporate America is sitting on right now. You can see post-pandemic that the figures have gone into the stratosphere. The trend was already on the rise since the Global Financial Crisis, when the U.S. government poured trillions of dollars into the system.

Trump’s tax cuts and a low-interest-rate environment allowed companies to score record profits and hold onto most of them. Then you can see during the pandemic they scored again and pocketed a historic amount of cash—all while increasing prices on the consumer to make sure they took what was in your pocket as well. Things cooled off a bit during that inflation spike when the consumer finally hit a wall, but as you can see, they’ve come back with a vengeance.

You might think that corporations are absolutely killing it by looking at this. But there’s more than meets the eye here. And it explains the relentless pace of stock buybacks.

According to the St. Louis Fed, corporate America came into the year with $209 billion in cash reserves. This kind of dough can be used to issue dividends to shareholders, invest in projects, pay down debt, bonus employees, invest in the market, chill for a rainy day—or to purchase back shares of its own company. That’s what we’re seeing thus far in 2025 in a rather significant way.

Corporate America has been so drunk on free Fed money for so long while getting used to fleecing the American consumer that it’s hiding the fact that they’re not as profitable as the cash-on-hand picture would indicate.

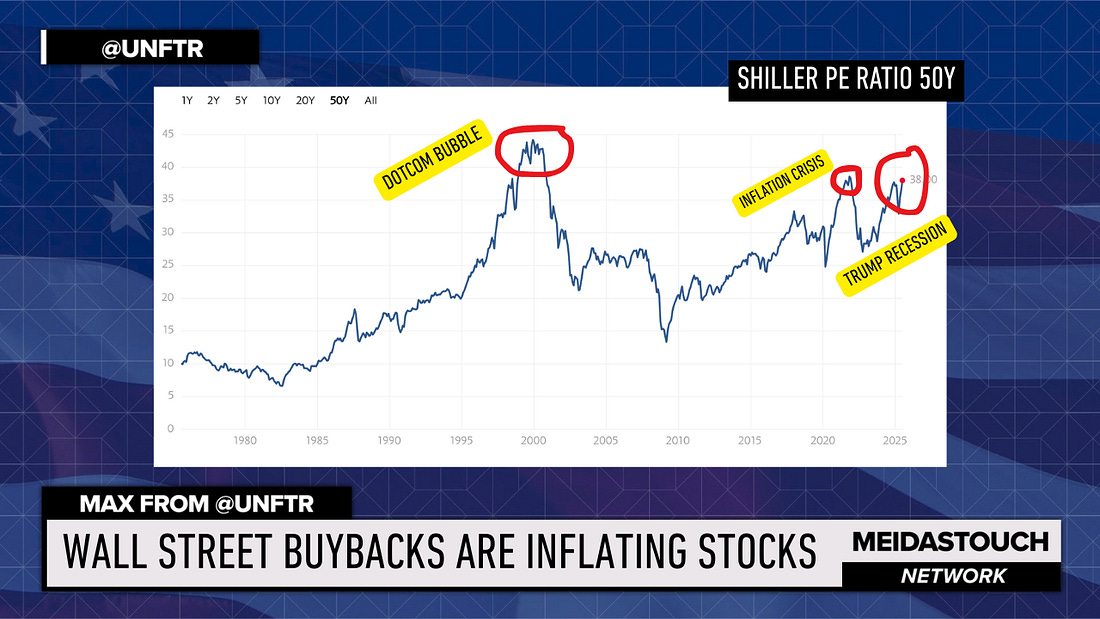

|

The Shiller PE ratio chart tracks earnings per share of public corporations on the S&P 500. Easiest way to understand this is: the higher the line on the chart, the less profitable a company is relative to its share price. You can see the first spike in 2000 is the dotcom bubble. (If you’re hesitant about the rush of capital into AI stocks, then you probably lived through this period.) This is when any company with .com at the end was flooded with investment money, even if it was a turd like Truth Social.

After that crash, PE ratios came back down to earth, and you can see the valley during the Global Financial Crisis. But as you know, the stock market has been on a never-ending climb since that time. You can see the two highlighted areas are the inflation crisis and right now—during what we need to start calling the Great Trump Recession because we’re already in it.

The stock markets are hitting record highs because investors have nowhere else to put money. So even when inflation was through the roof under the Biden administration, the market cranked. And it’s hitting all-time highs these days as well. But the Shiller chart shows in black and white that the Emperor is butt-naked right now, with PE ratios almost at pre-dotcom bubble peaks.

One of the ways companies are able to influence share price to make it look better than it is through stock buybacks—because it reduces the number of shares outstanding. It’s rampant these days, which is why the chart looks like that, and it’s really underhanded as well. So much so that it used to be illegal. Hold onto your hat when I tell you who made it legal.

Ronald Reagan.

I know, I know. Shocking, right?

In 1982, John Shad, the SEC chair under Reagan, implemented Rule 10b-18. This rule gave corporations a green light to repurchase their own shares without fear of being accused of market manipulation, as long as they followed some laughably permissive guidelines. It was deregulation at its finest—another win for the "free market" fundamentalists who dominated economic policy in the '80s. (And the ’90s. And the aughts. And today. Jesus, this is exhausting.)

Through the ’90s and into the 2000s, buybacks exploded. By the early 2000s, S&P 500 companies were spending more on buybacks than on dividends. By 2007, S&P 500 companies were spending nearly 90% of their earnings on share repurchases and dividends, leaving precious little for investment, research, or workers.

If Reagan-era deregulation opened the door to buybacks, it was a Clinton-era tax policy that turned them into an executive compensation bonanza.

In 1993, the Clinton administration pushed through Section 162(m) of the IRS tax code. Like so many “New Democrat” initiatives, on the surface it sounded like a progressive policy aimed at reining in excessive executive pay. The law capped the corporate tax deductibility of executive compensation at $1 million per executive for publicly traded companies.

Problem solved, right? Wrong. The law included a massive loophole: "performance-based" pay—such as stock options and certain bonuses—was exempted from the cap.

The results were exactly the opposite of what was ostensibly intended. Rather than limiting executive compensation, Section 162(m) caused it to explode. Companies simply capped base salaries at $1 million and shifted compensation to stock options and performance bonuses tied to—you guessed it—stock price.

An SEC study found that executives' sale of personally owned stocks increased from an average of $100,000 per day to $500,000 per day immediately following their companies' buyback announcements. In other words, corporate executives are using company money to pump up stock prices, then personally cashing out at those inflated prices.

Of course, Trump is the president and not the CEO, so executive compensation doesn’t matter to him. Nor does he actually control the shares.

Some other idiot does at the moment. (See above.) But the president is the sole beneficiary, so when the stock goes up, so does the value of the holding that will eventually come back to daddy.

So we’ve got the grift, which is the SPAC, inside the con, which is pumping value through buybacks, which leaves the shell game. It was only a matter of time, and now we know what it is.

The Scam Revealed

Should have seen it all along.

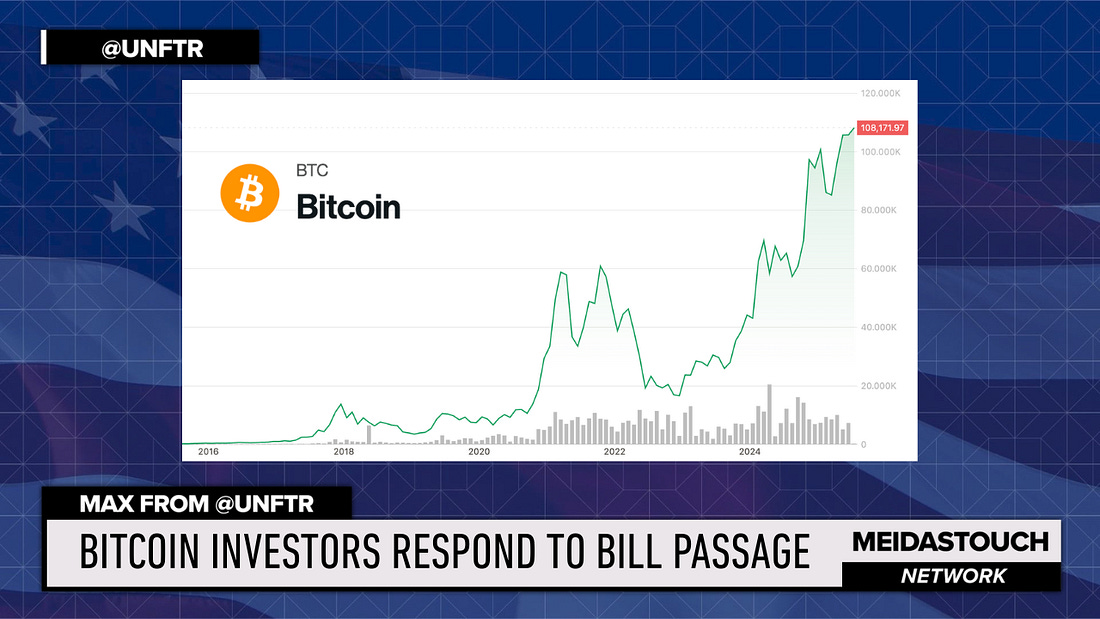

Whether the GOP gets anything done on crypto-specific regulations is a footnote. As you can see here…

|

The crypto market responded pretty enthusiastically to the passage of the Big Beautiful Bill for two very cynical reasons. The first is that very wealthy people are going to have more disposable income, which means they’ll be more inclined to invest in riskier assets. And because economic data is degrading rapidly and the Big Ugly Bill is going to obliterate consumer spending and drive us into a recession, speculative assets like gold and Bitcoin stand a good chance to see a flood of hedge investments.

So what does this have to do with Trump, the SPAC, and Truth Social?

Because Trump Media just filed paperwork seeking approval to launch an ETF to invest in Bitcoin and Ethereum. A little boost to the share price with the buyback to pad the pockets of the initial investors—and a plan to roll the remaining $2.5 billion into crypto investments. And with that, the shell game is revealed.

Max is a contributor to the MeidasTouch Network and Publisher of UNFTR Media. Watch Max’s video report on this topic by clicking here or watch at the top of this article.

For deeper dives into economic and socioeconomic stories, visit UNFTR.com or @UNFTR on YouTube. Make sure to sign up for the FREE weekly UNFTR newsletter here.

Resources

Yahoo Finance: Chamath Palihapitiya’s Crumbling SPAC Empire

Morningstar: How to Lose Money: Buy Digital World Acquisition Corp.

NYTimes: Trump Media Trust

SEC: Brian Shevland SEC

AFR: Luiz Philippe de Orléans e Braganza Profile

SPAC Insider: Digital World Drama

SPAC Insider: Benessere Capital

Inside Edition: Trump Media Stock (VIDEO)

Bloomberg: Stock Buyback Record Month

CNN: Betting on bitcoin as Trump boosts crypto